Key Points

-

Prior to the launch of ChatGPT, big tech’s capital expenditures were around $100 billion annually.

-

That figure is expected to rise to almost $500 billion by 2026 as the rapid buildout of data center infrastructure continues.

-

This dynamic will serve as a powerful tailwind for Nvidia as it continues to roll out more powerful new chip architectures.

- 10 stocks we like better than Nvidia ›

Prior to the launch of ChatGPT, big tech’s capital expenditures were around $100 billion annually.

That figure is expected to rise to almost $500 billion by 2026 as the rapid buildout of data center infrastructure continues.

This dynamic will serve as a powerful tailwind for Nvidia as it continues to roll out more powerful new chip architectures.

Over the past few years, many corporate budgets have been reoriented toward artificial intelligence (AI) investments. Nowhere is this shift more evident than among the cloud hyperscalers — Microsoft, Alphabet, and Amazon — as well as other tech titans like Meta Platforms and Oracle.

In just this year alone, Meta committed $14.3 billion to Scale AI and launched a new research hub, Meta Superintelligence Labs (MSL). It also signed a six-year, $10 billion agreement with Google Cloud. Meanwhile, Microsoft just struck a $17.4 billion deal with Nebius, a rising neocloud specialist.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

At the center of this unprecedented wave of AI infrastructure spending stands one clear beneficiary: Nvidia (NASDAQ: NVDA). Whether directly or indirectly, the graphics processing unit (GPU) powerhouse is capturing a significant chunk of the money being spent on AI infrastructure.

Let’s explore how big tech is reshaping the AI landscape — and why these secular tailwinds point to further significant upside for Nvidia.

AI infrastructure spending has accelerated since the launch of ChatGPT

The launch of ChatGPT in November 2022 ignited an unprecedented AI arms race among the world’s largest companies. What’s important to recognize is that their capital expenditures in this battle are not plateauing — they’re accelerating.

AMZN Capital Expenditures (TTM) data by YCharts.

Data from Goldman Sachs underscores just how dramatic these dynamics have become. In 2021, Alphabet, Meta, Amazon, and Microsoft collectively had capex of about $100 billion. By next year, Wall Street expects that figure to approach nearly $500 billion.

What does this mean for Nvidia?

Training and deploying large language models (LLMs) and building generative AI applications demands extraordinary amounts of computing power. GPUs are parallel processors, which makes them some of the best chips available to provide the type of computing power AI workloads require. Today, Nvidia commands a more than 90% share of the GPU market, giving it a dominant position within the AI supply chain.

A significant portion of the AI capex surge is flowing directly into GPUs and the supporting data center equipment necessary to maximize their performance.

This dynamic places Nvidia in a uniquely enviable position as the backbone of modern AI development — and it’s poised to capture incremental budget allocations as hyperscalers and other data center operators race to secure its next-generation chips the moment they become available.

Image source: Getty Images.

Is Nvidia stock a buy?

The magnitude of hyperscaler infrastructure investment reflects more than the world’s apparently insatiable appetite for AI computing power. It underscores a deeper reality: AI is becoming the central growth engine for these companies, and securing access to the most advanced chips has shifted from being a matter of technological advantage to being a matter of competitive survival.

The accelerating pace of this spending suggests that corporations are still in the early stages of implementing their AI playbooks. Far from being a speculative bubble, this wave of infrastructure investment is the result of deliberate, long-term strategic planning by some of the world’s most influential companies as they pivot away from their traditional priorities and take on sophisticated projects in robotics, autonomous systems, cybersecurity, and more.

For Nvidia, this dynamic should translate into sustained pricing power for its wares, durable recurring demand, and a multiyear runway for rapid growth. Its GPUs and CUDA software platform have become the gold standard for enterprise AI tech stacks.

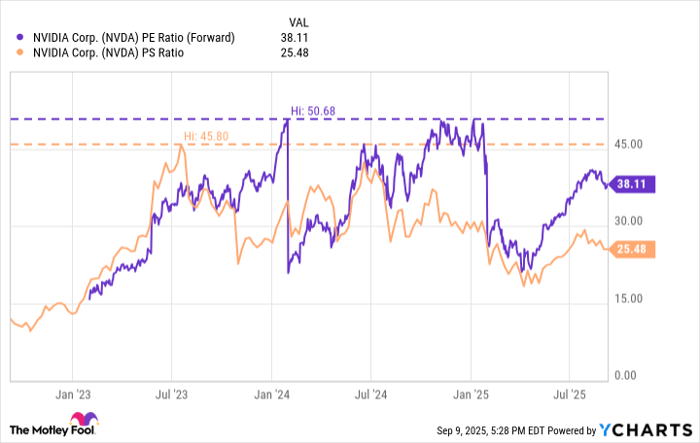

NVDA PE Ratio (Forward) data by YCharts.

Taken together, these tailwinds suggest that Nvidia could experience meaningful valuation expansion from here. As the infrastructure chapter of the AI narrative continues to unfold, Nvidia appears well positioned to remain as a core enabler of big tech’s transformation.

For these reasons, I see Nvidia stock as a no-brainer investment, and view it as one of the most compelling buy-and-hold opportunities in the market.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $649,037!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,086,028!*

Now, it’s worth noting Stock Advisor’s total average return is 1,056% — a market-crushing outperformance compared to 188% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of September 8, 2025

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Goldman Sachs Group, Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Fool recommends Nebius Group and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

#Amazon #Microsoft #Alphabet #Meta #Delivered #Trillion #Dollars #Worth #Great #News #Nvidia #Investors