Key Points

-

Snowflake developed the revolutionary Data Cloud, which helps businesses unify their valuable information even if it’s siloed in different cloud platforms.

-

Snowflake now offers an expanding portfolio of tools to help businesses develop artificial intelligence (AI) software.

-

Snowflake’s revenue growth accelerated during its recent quarter, but its stock is trading at a sky-high valuation that could limit further upside.

- 10 stocks we like better than Snowflake ›

Snowflake developed the revolutionary Data Cloud, which helps businesses unify their valuable information even if it’s siloed in different cloud platforms.

Snowflake now offers an expanding portfolio of tools to help businesses develop artificial intelligence (AI) software.

Snowflake’s revenue growth accelerated during its recent quarter, but its stock is trading at a sky-high valuation that could limit further upside.

Large organizations tend to use multiple cloud computing platforms like Microsoft Azure and Amazon Web Services to manage their day-to-day operations. This leads to fragmented data, meaning valuable information which is stored on one platform isn’t easily accessible on another, making it difficult to analyze.

Snowflake (NYSE: SNOW) created the Data Cloud to solve that problem. It sits on top of other cloud platforms and enables businesses to bring all of their data together in one place, where it can be analyzed more effectively to extract actionable insights. This also places Snowflake in a fantastic position in the artificial intelligence (AI) race, because businesses need easy access to all of their data to develop the best models.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Snowflake recently released its financial results for its fiscal 2026 second quarter (ended July 31), and a combination of accelerating revenue growth and a record order backlog sent its stock soaring by 20% in the aftermath. Should investors chase the rally, or wait for a better entry point?

Image source: Getty Images.

An expanding portfolio of AI products

Snowflake launched a new platform called Cortex AI in 2023, which provides businesses with access to ready-made large language models (LLMs) from the industry’s top developers, including OpenAI’s latest GPT-5. Businesses can plug their internal data into these models via Cortex, in order to develop AI software.

The platform also offers several tools to make data gathering easier. For example, Document AI can extract data from unstructured sources like contracts and invoices so it can be used to train models. Then there are Cortex Agents, which can be trained to autonomously complete different tasks — for instance, an agent can be trained to analyze transcripts of conversations between salespeople and customers to identify opportunities to generate more revenue.

Snowflake has another AI platform in public preview (testing) right now called Snowflake Intelligence. It allows businesses to “talk” to their data using natural language rather than programming language, which is a game changer because it means even non-technical employees can rapidly parse mountains of information to unlock valuable insights.

Snowflake had 12,062 total customers at the end of the fiscal 2026 second quarter, and more than 6,100 of them are using at least one of the company’s AI products every week.

Revenue growth just accelerated, but losses are piling up

Snowflake generated $1.09 billion in product revenue during the second quarter, comfortably beating management’s guidance of $1.04 billion. It was a 32% increase from the year-ago period, which marked an acceleration from the 26% growth the company delivered in the first quarter. Snowflake’s revenue growth had been decelerating each quarter for the last couple of years, so this was a welcome change.

The company’s net revenue retention rate ticked higher sequentially, which contributed to the strong result. It came in at 125%, which meant customers were spending 25% more money than they were at the same time last year, so some of the cloud giant’s investments in new AI products is paying off.

Snowflake’s remaining performance obligations (RPOs) also jumped 33% year over year to a record high of $6.9 billion. RPOs are like an order backlog reflecting customers’ planned future spending, so they are a good indicator of demand.

But it wasn’t all good news in Q2, because Snowflake continued to lose truckloads of money. It burned $298 million at the bottom line on a GAAP (generally accepted accounting principles) basis during the quarter, and while that was a modest improvement from its year-ago net loss, it carried the company’s total net loss for the first half of fiscal 2026 to a record $728 million. That puts Snowflake on track to exceed its $1.3 billion loss from fiscal 2025.

The Q2 situation looked much better on a non-GAAP basis, because it excluded the whopping $436 million worth of stock-based compensation that went to employees. The company was profitable to the tune of $129 million by that measure during the quarter, more than doubling its year-ago result.

But investors shouldn’t ignore stock-based compensation, because despite being a non-cash expense, it dilutes the holdings of existing shareholders, which can dent their potential returns.

Snowflake’s valuation could limit its upside from here

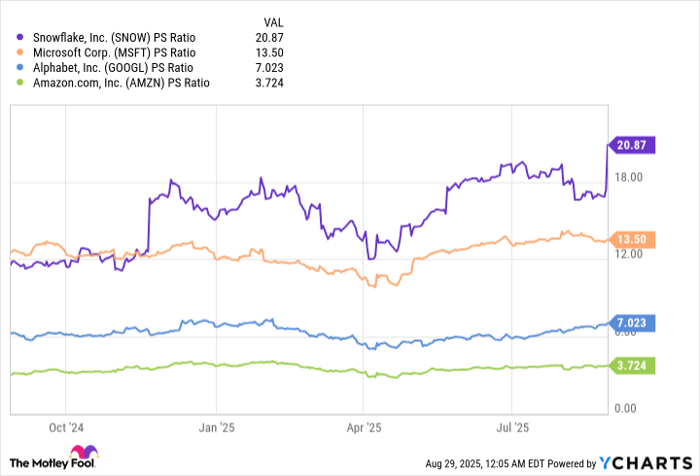

Valuation might be the biggest reason to be cautious about Snowflake stock right now. It’s trading at a price-to-sales (P/S) ratio of 20.8, which is not only a one-year high, but it makes Snowflake significantly more expensive than each of the major cloud providers:

SNOW PS Ratio data by YCharts

Microsoft, Amazon, and Alphabet operate several other businesses beyond the cloud, so they aren’t the perfect comparisons to Snowflake. However, 20 times sales is expensive for almost any stock, except maybe a premium AI name like Nvidia, which has more than tripled its quarterly revenue since the AI revolution started gathering momentum around two years ago.

Therefore, despite the strength of Snowflake’s business right now, its valuation might be a barrier to further upside in the near term. Investors who buy the stock today can still do well, but they might have to commit to a holding period of five years or more to maximize their chances of earning a positive return.

Should you invest $1,000 in Snowflake right now?

Before you buy stock in Snowflake, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Snowflake wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $651,599!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,067,639!*

Now, it’s worth noting Stock Advisor’s total average return is 1,049% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of August 25, 2025

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, Nvidia, and Snowflake. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

#Snowflake #Stock #Buy #Answer #Surprise