Key Points

-

Hyperscalers like Microsoft are beginning to invest in cloud-based GPU infrastructure to broaden capacity requirements.

-

Oracle and CoreWeave are currently the major players in the infrastructure-as-a-service industry.

-

Nebius Group is a smaller yet formidable competitor to GPU service incumbents.

- 10 stocks we like better than Nebius Group ›

Hyperscalers like Microsoft are beginning to invest in cloud-based GPU infrastructure to broaden capacity requirements.

Oracle and CoreWeave are currently the major players in the infrastructure-as-a-service industry.

Nebius Group is a smaller yet formidable competitor to GPU service incumbents.

For the first time since artificial intelligence (AI) captured Wall Street’s imagination, investors are beginning to broaden their scope beyond the “Magnificent Seven.” Two names that have attracted growing attention this year are Oracle and CoreWeave.

Unlike the tech titans that dominate headlines, Oracle and CoreWeave are carving out their niche at the infrastructure layer of the AI ecosystem. The opportunity they’ve identified is straightforward but also mission-critical: providing cloud-based access to GPUs. These chips — designed primarily by Nvidia and Advanced Micro Devices — remain supply constrained as they are largely absorbed by the world’s largest companies.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

This supply imbalance has created an opportunity to enable AI model development by offering GPUs as a service — a business model that allows companies to rent chip capacity through cloud infrastructure. For businesses that cannot secure GPUs directly, infrastructure services are both time-saving and cost-efficient.

In the background, however, a small, albeit capable, company has been competing with Oracle and CoreWeave in the GPU-as-a-service landscape. Let’s explore how Nebius Group (NASDAQ: NBIS) is disrupting incumbents and why now is an interesting time to take a look at the stock for your portfolio.

17.4 billion reasons to pay close attention to Nebius

Last week, Nebius announced a five-year, $17.4 billion infrastructure agreement with Microsoft. For reference, up until this point, Nebius’ management had been guiding for $1.1 billion in run rate annual recurring revenue (ARR) by December. I point this out to underscore just how transformative this contract is in terms of scale and duration.

The Microsoft deal not only places Nebius firmly alongside peers like Oracle and CoreWeave in the AI infrastructure conversation, but it also serves as validation that its technology is robust enough to meet the standards of a hyperscaler.

For Microsoft, the partnership is equally strategic. With GPUs in chronically short supply and long lead times to expand data center capacity, this agreement allows Microsoft to secure adequate compute resources without stretching internal infrastructure or assuming the upfront capital expenditure (capex) budget and execution risks that come with it.

Image source: Getty Images.

Why this deal matters for investors

AI investment is not a cyclical trend — it’s a structural shift. Enterprises are deploying applications into production at unprecedented speed, workloads are scaling rapidly, and new use cases in areas like robotics and autonomous systems are emerging.

For companies that supply the compute underpinning this increasingly complex ecosystem, these dynamics create durable secular tailwinds. By securing Microsoft as a flagship customer, Nebius has established itself within this foundational layer of the AI infrastructure economy.

Is Nebius stock a buy right now?

Since announcing its partnership with Microsoft, Nebius shares have surged roughly 39% as of this writing (Sept. 16). With that kind of momentum, it’s natural to wonder whether the stock has become expensive. To answer that, it helps to put its valuation in context.

Prior to the Microsoft deal, Nebius was guiding for $1.1 billion in ARR by year-end. If I assume Microsoft’s $17.4 billion commitment is evenly spread across five years (2026 to 2031), that adds about $3.5 billion annually — bringing Nebius’ pro forma ARR closer to $4.6 billion.

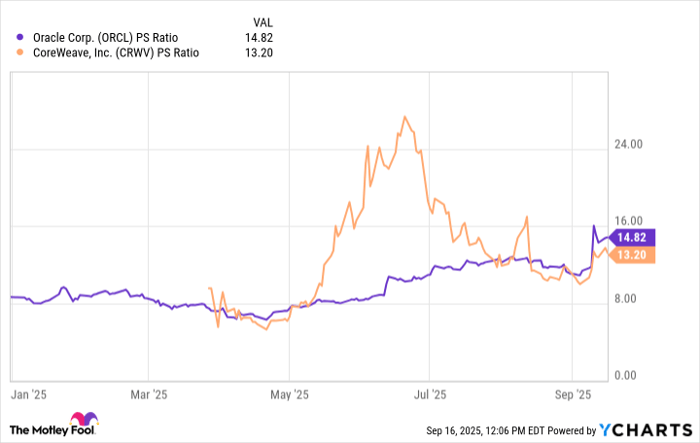

Against its current market cap of $21.3 billion, Nebius stock trades at an implied forward price-to-sales (P/S) ratio of 4.6. On the surface, that looks meaningfully discounted to peers like Oracle and CoreWeave.

ORCL PS Ratio data by YCharts

That said, there are important caveats to consider. My analysis assumes no customer attrition over the next several years — this is unrealistic due to competitive pressures. While Nebius may continue winning large-scale contracts, it’s also reasonable to expect some customer churn.

Moreover, comparing Nebius’ future ARR to Oracle’s and CoreWeave’s current revenue base is not an apples-to-apples match. Oracle, for example, has reportedly inked a $300 billion cloud deal with OpenAI. Meanwhile, CoreWeave also has multiyear, multibillion-dollar commitments tied to OpenAI. The catch is that OpenAI itself doesn’t have the cash on its balance sheet to fully fund these agreements — leaving questions about their viability.

In short, Nebius appears attractively valued relative to its peers — but the landscape is evolving quickly and riddled with moving parts. The more important takeaway is that Nebius is now winning significant business alongside its brand-name peers.

In my eyes, this validation in combination with ongoing structural demand tailwinds makes Nebius a compelling buy and hold opportunity as the AI infrastructure narrative continues to unfold.

Should you invest $1,000 in Nebius Group right now?

Before you buy stock in Nebius Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nebius Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $651,345!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,080,327!*

Now, it’s worth noting Stock Advisor’s total average return is 1,058% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of September 15, 2025

Adam Spatacco has positions in Microsoft and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Microsoft, Nvidia, and Oracle. The Motley Fool recommends Nebius Group and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

#Microsoft #Gave #Investors #Billion #Reasons #Buy #Monster #Artificial #Intelligence #Data #Center #Stock #Hand #Fist