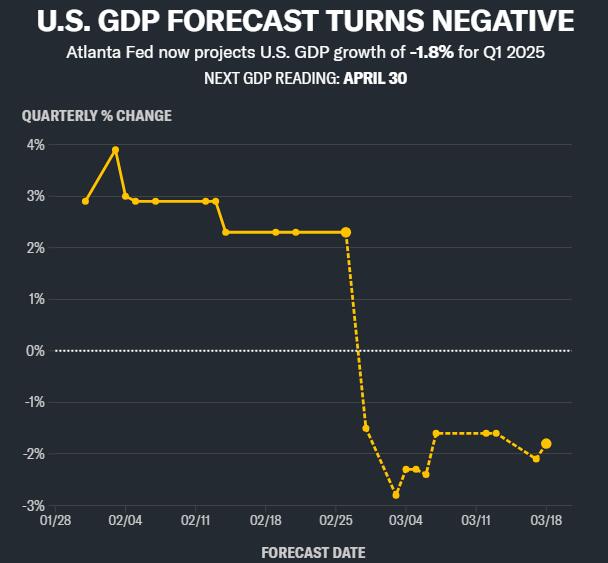

The stock market faces a pivotal question: Is the current U.S. economic slowdown a temporary dip or the precursor to a recession? A “soft landing” scenario, with continued albeit slower growth, may be largely priced into stocks. However, a “hard landing” – a recession driven by reduced spending, tariffs, and tax cut uncertainty – is likely not fully reflected in market valuations. Anecdotal evidence from corporate leaders, along with concerning comments on earnings calls from companies like FedEx and Nike, points to increasing economic anxieties. Strategists like JPMorgan’s Bruce Kasman (40% recession probability) and BCA Research’s Peter Berezin (75%) have issued high recession warnings. Recent disappointing retail sales data and weak consumer confidence further suggest a weakening economic outlook, adding pressure on the stock market to price in a potentially more negative scenario.

A critical question looms over the stock market: Is the U.S. economy experiencing a temporary slowdown, or is it heading towards a full-blown recession?

One perspective suggests that the current economic deceleration represents a brief downturn, followed by a period of continued, albeit slower, growth. This scenario reflects economic resilience amidst significant policy uncertainty stemming from Washington. It could be argued that the stock market has largely factored in this “soft landing” scenario.

The alternative, and more concerning, possibility is that the slowdown will escalate into a recession. Businesses and consumers may curtail spending due to factors like escalating tariffs and uncertainty surrounding the extension of Trump’s tax cuts. This “hard landing” scenario, arguably, is not fully reflected in current stock prices.

Anecdotal evidence supports both narratives. A CEO of a major consumer goods company recently expressed to me a sense of general economic sluggishness. Similarly, a beverage company CEO indicated that the ongoing trade war with China is prompting a reevaluation of their spending plans for the coming years.

Adding to the recessionary concerns, JPMorgan strategist Bruce Kasman recently estimated a 40% probability of a recession this year. This is among the highest such predictions on Wall Street, surpassed only by BCA Research’s Peter Berezin, who places the probability at 75%.

These concerns aren’t confined to private conversations or exclusive research reports. They are increasingly surfacing in the earnings releases and conference calls of publicly traded companies. And the market is reacting swiftly, seemingly pricing in something more severe than a mere slowdown.

For instance, FedEx CEO Raj Subramaniam, on the company’s recent earnings call, acknowledged “uncertainty to demand” due to the “evolving market.” Another FedEx executive specifically mentioned uncertainty within the “industrial economy.”

Nike’s recent earnings call provided another stark reminder of economic realities. The company, a bellwether for consumer spending, is not immune to global trade tensions. Nike’s guidance for the upcoming quarter was particularly concerning, with projected sales declining by a mid-teens percentage—worse than analyst expectations. Profit margins are also expected to be squeezed due to tariffs and increased discounting.

Nike’s new CEO, Elliott Hill, prominently mentioned “economic uncertainty” early in the earnings call.

Recent economic data further reinforces the narrative of a weakening economy. U.S. retail sales in the previous month were significantly below expectations, adding to concerns raised by weak consumer confidence data and various Federal Reserve activity surveys.